Corporations have 3 important features...

1) They are legally distinct from the owners and pay their own taxes.

2) Corporations provide limited liability (owners are not held responsible for the firm's debt).

3) Owners are not usually the managers.

Financial Managers' role in Corporations...

1) Making Investments or Capital Budgeting decisions (What real assets to buy).

2) Financing Decisions (How to raise the necessary cash).

CFO: Responsible for overall Financial policy and Corporate planning.

Treasurer: Responsible for Cash Management, Raising Capital, Banking Relationships.

Controller: Responsible for Preparation of Financial statements, Accounting, Taxes.

Principal-Agent Problem:

Shareholders (owners) want managers to increase the value of the company's stock. While managers may have different objectives. This is called Principal-Agent problem.

Note: Information taken from "Principles of Corporate Finance" by Brealey, Myers and Allen.

Sunday, October 08, 2006

Saturday, October 07, 2006

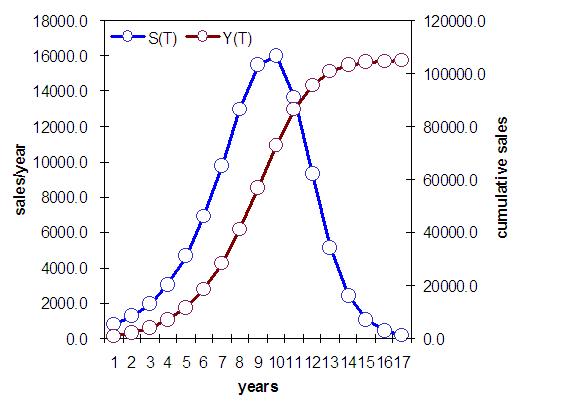

Bass Diffusion Model

Bass diffusion model is used to predict the demand forecast of a new product or service. First presented by Frank Bass in 1969, this model incorporates the effect of how information about a product is communicated between members of a social system.

Why is it needed?

Predicting the demand of a new product is very critical for any company. For example companies have to decide how much of the new product to produce in order to meet the demand initially and in the months and years ahead. Another decision for the company is to determine how much to offer in promotional discounts or price cuts and the effects of these in speeding the adoption of the new product. Even investments companies use this model to rougly determine whether or when to invest in the company. They can determine when the sales would peak so that they can take their money out based on that information.

Parameters

"m", total market size. This should be all inclusive. It is usually the total consumer base, total number of households etc depending on the nature of the product or service.

"p", coefficient of innovation (rate or probability that an innovator will adopt in time t.)

"q", coefficient of imitation (this accounts for the "word of mouth" or "social contagion" effect that result from interpersonal communications between adoptors and non-adoptors.

Variables

S(t), number of new adopters in time time period t

N(t), total or cumulative adopters through period t

N(t-1), cumulative adopters through previous time period t-1

Model

S(t) = [p + (q/m) N(t-1)] [m-N(t-1)] = number of new adopters during time t

Estimating parameters

m, can be estimated by surveys, census figures etc.

p and q can be determined by analyzing the adoption of previously launched analogous products. Other approach is to derive p and q by using non-linear least squares (NLLS) methods from early actual unit sales data.

Information taken from "Forecasting the adoption of a New Product", a Harvard Business School class note (9-505-062)

Tuesday, October 03, 2006

NPV vs IRR

Today was the first class in Corporate Finance. The Professor is really good. Excellent in teaching. He, however, warned that things will look simpler during the class but unless we work out the practice problems, we will be doomed... :(

Some key takeaways:

1) Differences between real and nominal interest rate. (nominal = real + inflation). Real interest rate will always be positive as long as the economy is productive.

2) Different types of valuation: NPV (net present value), IRR (internal rate of return), Payback and discounted payback and Book rate of return. NPV is by far the best way to value the present value (PV) of an investment.

3) Cash flow = EBIT + Dep & Amortization - Increases in net working capital - CapEx + Proceeds from Asset sales - Realized cap gain taxes + Realized cap loss savings - EBIT*Tax rate

4) "All valuations involve comparisons".

Subscribe to:

Posts (Atom)